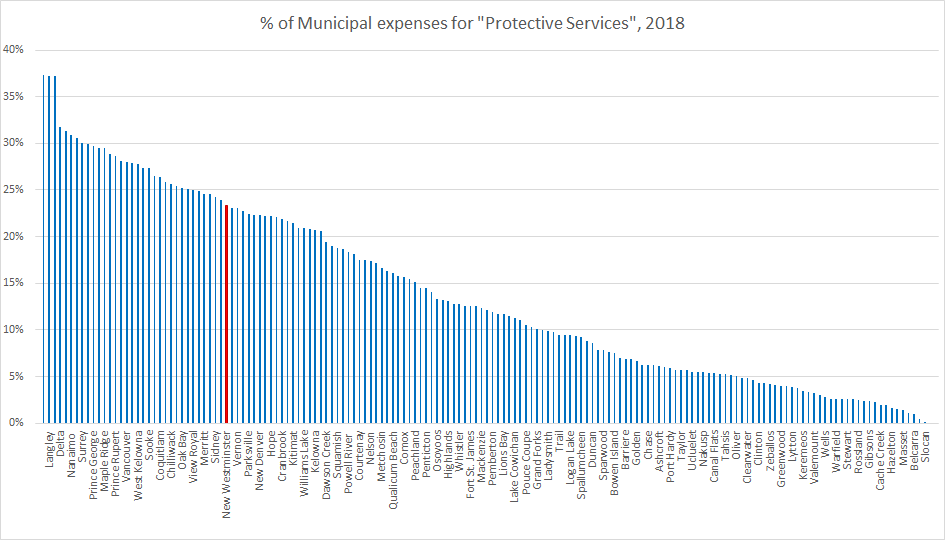

In my last post, I tried to give some data on how policing works in BC and New Westminster, and I tried to do so without opining, recognizing that my own biases and opinions probably sneak in all over everything I write.

There was one asterisked statement in that post I wanted to follow up on, because it relied on a more detailed reading of the Police Act, and that post was long enough without this extra 1,000-word digression. However, in the day or two since I started sketching out that previous post, there has been much news, including the Mayor of Vancouver saying he really can’t do much about policing costs, some in the chattering class suggesting that was artless dodging, and the Solicitor General and Premier saying the Police Act is due for an update. All of the sudden, that asterisked point became the center of debate, so I will try to unpack a bit here.

Again, by means of caveat: I am not a lawyer or specialist in interpreting legal documents. I am not on the Police Board, so operating under the Police Act is not part of my day-to-day. I may get details wrong here, and please correct me if I do.

The Police Act says that a municipality over 5,000 residents must pay for policing. At first blush, that means City Council is responsible for approving the Police Budget (both operational and their capital requests) as part of their annual budget work, and we do that. However, that is not the entire story.

Section 15 of the Police Act says:

…a municipality …must bear the expenses necessary to generally maintain law and order in the municipality and must provide, in accordance with this Act, the regulations and the director’s standards, policing and law enforcement in the municipality with a police force or police department of sufficient numbers to adequately enforce municipal bylaws, the criminal law and the laws of British Columbia, and to maintain law and order in the municipality, adequate accommodation, equipment and supplies for the operations of and use by the police force or police department

This makes clear that the Provincial Government has ultimate authority to determine the level to which police are funded in BC. Section 17 of the Act follows up by saying the Director of Police Services (a Provincial Government employee appointed by the Solicitor General, see Section 39 of the Police Act) must notify the City they are in breach and direct them to fix it. If they fail to do so, the Solicitor General can fix it, and send the municipality the bill.

Section 26 also puts policing costs at the foot of the Police Board:

Subject to a collective agreement as defined in the Labour Relations Code, the chief constable and every constable and employee of a municipal police department must be employees of the municipal police board, provided with the accommodation, equipment and supplies the municipal police board considers necessary for his or her duties and functions, and paid the remuneration the municipal police board determines.

Then Section 27 lays out the slightly-convoluted response if the Council refuses to pay for something the Police Board asks. The Board or Council may appeal to the Director (that Provincial government employee), who determines “whether the item or amount should be included in the budget”, and reports back, cc’ing the Solicitor General. If ordered so, the Council must include the item in its budget, or be in violation of the Police Act. Naturally, a lot rides on that should above, but ultimately, the Solicitor General holds all the cards in this dispute.

The grey ares in the middle of all this is the determination of what “sufficient numbers” and “adequate” are in the sections above. How does one measure if the level of service planned by the Police Board and funded by the Council is sufficient? Or more to the point, how would one know when it is insufficient?

This brings us to Regulations, which are pieces of Legislation that exist under Acts. Again, not a lawyer here, but Acts are high level documents enacted by the Legislature that set out general principles and duties, establishing the will of the Government. Regulations are subordinate to and empowered by Acts, but include a lot of the fuzzy details that often need adjustment without opening up the entire big Act. A probably-wrong but simplified example: an Act would say “driving above a speed limit is illegal”, where the subordinate Regulation would say “Speed limits on urban roads is 50km/h unless otherwise designated”.

In Section 74, the Police Act gives the “Lieutenant Governor in Council” (a fancy way to say, the government of the day) the power to create Regulations on various aspects of the Act, including:

prescribing the minimum salary or other remuneration and allowances to be paid to members of police forces, police departments, designated policing units or designated law enforcement units” and “prescribing the minimum number of members of police forces, police departments and designated policing units that are to be employed on a basis of population, area or property assessment, on any combination of them, or on another basis

To the best of my knowledge, these regulations do not actually exist (a list of regulations that do exist under the Police Act is available here). Police staff numbers and police remuneration are determined by the Board, the latter approved by the Council, and Regulations just don’t come into it. There is, however, a legal ability for the provincial government to create such regulations if needed to clarify the funding required for “adequate” policing. Short those regulations, if a dispute occurred and persisted, it would likely end up in the Courts and a judge would decide, though my (unskilled) reading of the Act suggests it would be the Police Board whose opinion carries the most weight.

In in my time on Council in New Westminster, there has never been a significant conflict between the Board and Council on the budget. Council has, on several occasions, reviewed budget augmentation requests made by the Police as part of our annual budgeting process and sent some back for review. This type of negotiation has always resulted in agreed-upon operational budget and Capital requests, much like in other departments in the City from Engineering to Parks.

Yes, a Municipal Council could push back hard against a Police budget and significantly reduce it. Yes, the Police Board could appeal to the provincial government if they feel this reduction would not allow them to discharge their duty under the Police Act to “enforce municipal bylaws, the criminal law and the laws of British Columbia; maintain law and order in the municipality; and prevent crime”. Then the ball would firmly be in the provincial government’s court to determine the path forward – accept that Council’s reductions or order the Council to pay. No doubt, Politics would ensue.